Manage Your Business

How to Calculate the Cost of Goods Manufactured (COGM)?

The Cost of Goods Manufactured is a great way to see production costs and their impact on your bottom line. It allows managers to identify cash leaks and adjust prices to ensure that the business is developing.

What is the cost of goods manufactured?

The Cost of Goods Manufactured is an accounting term that indicates the total cost of producing products and transferring them into finished good inventory within a given accounting period.

COGM does not account for products that are either ready or have been sold. It is therefore a useful tool to see the whole picture of production costs and determine the profitability of a company.

What is the importance of the Cost of Goods Manufactured?

COGM, as mentioned above, is a great way to see how your production costs relate to profitability. You can increase your bottom line by knowing the COGM and making adjustments as necessary.

Knowing the COGM can also help companies:

Better manage your inventory

- – keep better financial records

- – develop better pricing strategies

- – track business development.

These benefits make COGM a key KPI in every manufacturing company.

Cost of Goods Manufactured and Total Manufacturing Cost

Both the Total Manufacturing Cost and Cost of Goods Manufactured are related terms. The Total Manufacturing Cost includes the direct material and labor costs as well as overhead costs. However, the Cost of Goods Manufactured also takes into account the changes in Work-in Progress Inventory.

However, the Total Manufacturing Cost is only a fraction of the Cost of Goods Manufactured.

How do you calculate the cost of goods manufactured?

The COGM includes all costs associated with making finished products.

Direct materials. Calculating the direct material cost can be done by adding the starting raw materials inventory to the end raw materials inventory and subtracting it.

The wages of employees who directly deal with production activities (i.e. The shop floor workers.

– Production overhead devoted to the production. Indirect materials are materials that are used in production, but not necessarily part the product. glue, sandpaper, lubricant, etc. (); indirect labor, such as supervision, quality control, materials administration, and other workers that are not directly involved in the production of goods, but without whom production wouldn’t happen; depreciation on the premises and equipment; rent or property taxes; insurance.

The Total Manufacturing Cost includes all of the costs mentioned above.

The Beginning WIP inventory is also included in the COGM. The cost of goods that were not finished during the accounting period.

To calculate COGM simply add the Beginning WIP inventory to the Total Manufacturing cost and subtract the Ending WIP inventory. This will give the total cost for the goods that were completed during the specified time period.

Exemple

A furniture manufacturer may have $12,000 worth of furniture at the beginning of each quarter. This is the Beginning WIP inventory.

Starting WIP Inventory = $12,000

The company also has $8,000 worth raw materials on hand, ready to be turned into furniture. The raw material inventory is replenished by $5,000 of stock within the quarter. The stock remaining as raw materials at the end of each quarter is $3,000 These figures allow us to calculate the Direct Materials used.

Direct Materials = $8,000 + $5,000 – $3,000 = $10,000

Eight shop floor workers are employed by the company and are responsible for the execution production processes. The four senior workers earn $2,600 per month and the four others make $2,200 each month. We calculated their three-month salaries as the sum (since we used a quarter of the accounting period to calculate the amounts). The Direct Labor Costs are the sum of their three-month salaries (as we decided that the accounting period for the calculations is a quarter, i.e.

Direct Labor = (($2,600×4) + ($2,200×4)] x3 = ($10,400+ $8,800)x3 = ($10,400+ $8,800). x3 = $19,200×3 = $57,600

Manufacturing overhead is $28,600. It includes indirect labor costs such as maintenance (wages $9,000 per quarter) and warehouse (wages 12,000 per quarter), additional materials like glue and sandpaper (800), rent (6,000 per quarter), insurance (200 per quarter), and equipment depreciation (i.e. $2,400 per year). $600 per quarter.

Manufacturing Overhead = $28,600

The quarter’s Total Manufacturing Cost is therefore the sum of direct material and labor costs plus manufacturing overhead.

Total Manufacturing cost = $10,000 + $57 600 + $28,600 = $96,200

Furniture worth $11,000 was still being produced at the end of quarter. This is the Ending WIP inventory.

Ending WIP Stock = $11,000

Finally, the Cost of Goods Manufactured is calculated by adding the Beginning WIP inventory to the Total Manufacturing Cost, and subtracting from the Ending WIP inventory.

COGM = $12,000 + 96,000 – $11,000 = $97.200

These basic calculations show that the quarterly COGM for the furniture company is 97.200 dollars.

Cost of Goods Manufactured and Sold Cost of goods sold

Although the COGM and COGS are very similar terms, they should not be confused.

The Cost of Goods Manufactured is a measure of the finished products that have been sold as well as those that are still in stock. However, the Cost of Goods Sold only includes the cost of manufacturing the products during the accounting period.

COGM, however, is part of the COGS calculation in periodic inventories.

The previous example shows that if the company had a $10,000 starting inventory and a $20,000 end finished goods inventory, the COGS would be:

COGS = 10,000 + $97,200- $20,000 = $87,000.

For many reasons, the COGM and COGS may differ from one another.

During the accounting period, more items were manufactured than sold (i.e. Some items remain in stock and are awaiting sale.

– More items were sold than were produced in the accounting period (i.e. Some items were sold using the remaining finished goods inventory from the previous period.

Some finished goods and WIP inventory are no longer in demand. There is no market for these products anymore.

COGM in Manufacturing ERP

A proper MRP system can track different manufacturing costs and calculate both the COGM as well as the COGS if it is provided with accurate inputs. This perpetual inventory system eliminates a lot of the work involved in accounting and frees up time that can be used for other purposes.

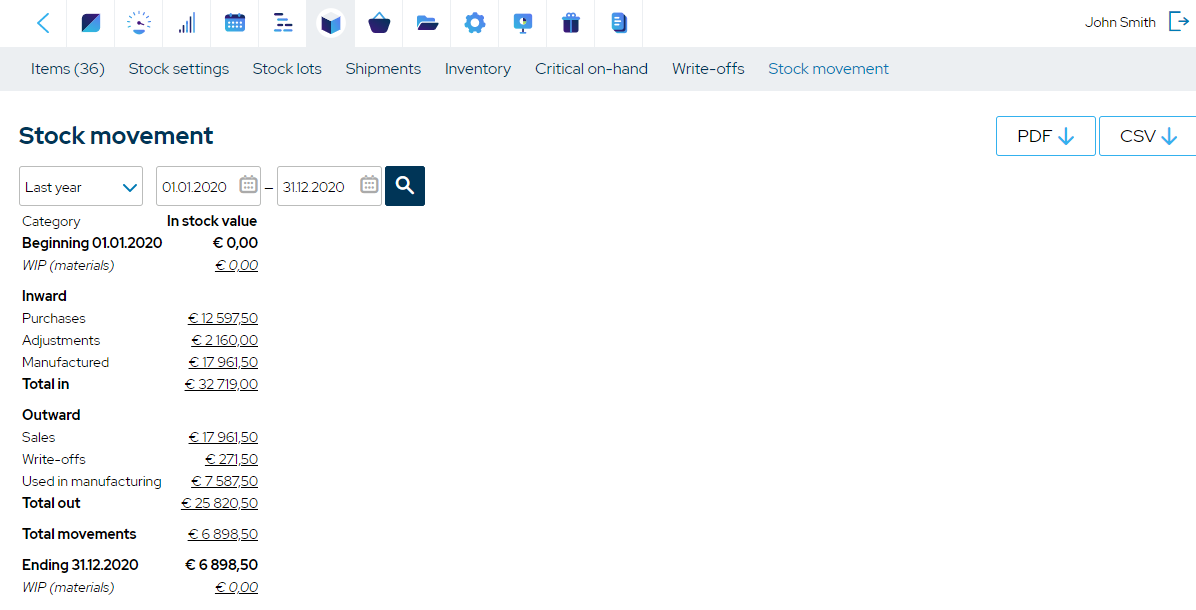

Managers can also use MRP software to monitor other KPIs such as overall equipment efficiency, manufacturing cost per unit, OTIF, and so on. In MRPeasy COGM is listed as the “Manufactured” field in Stock -> Stock movement-> Inward.

Conclusion

The Cost of Goods Manufactured (COG) is an important KPI. It can be used to measure the production costs of a manufacturing company and to identify problems and make improvements.

It is related to the Total Manufacturing Cost as well as the Cost of Goods Sold. However, the COGM is an independent concept with distinct purposes.

The COGM formula includes the Total Manufacturing Cost and the beginning and end WIP inventory. However, the Cost of Goods Sold incorporates both the COGM and the inventory.

An MRP system is a perpetual inventory system that helps manufacturing companies track manufacturing costs and calculate various KPIs automatically, including the COGM.

{kind=link}

Preventing Local Malware Injection in AI Apps

Blur Card – Crypto Cards with Hidden Fees

Nudefusion AI App Review

ControlNet: Revolutionizing Neural Control in AI Image Generation

PayPal Sports Betting Guide for Beginners

Nudefusion AI App Review

Blur Card – Crypto Cards with Hidden Fees